Deductions are items which are reduced from Taxable Salary to arrive at Income from Salaries

Taxable Salary

Less

Deductions

=Income from Salary

For Computing Income from Salaries.

- First we add all Taxable Allowances and Perquisites

- Then we calculate Deductions under Section 16 to arrive at Income from Salaries

Step 1 - Step 2 is Income from Salaries

There are basically 3 deductions

- Standard Deduction [ Section 16(ia) ]

- Entertainment Allowance [ Section 16(ii)]

- Professional Tax [ Section 16(iii)]

All these deductions are reduced to arrive at Income from Salary

Format

| Particulars | Amt. received | Exempt | Taxable |

| Basic Salary | xx | xx | xx |

| +Taxable Allowance | xx | xx | xx |

| +Taxable Perquisites | xx | xx | |

| Gross Taxable Salary | xx | ||

| Less | |||

| Deductions | |||

| Standard Deductions | xx | ||

| Entertainment Allowance | xx | ||

| Professional Tax | xx | ||

| Income from Salary | xx |

Lets study these 3 deductions one by one

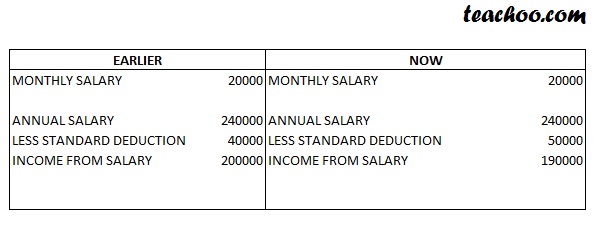

New Standard Deduction under Section 16(ia)

( Applicable for F.y 2018-19, A.Y 2019-20 onwards)

Deduction under section 16(ia) states that a taxpayer having income chargeable under the head 'Salaries' shall be allowed a deduction of Rs. 50,000

or the amount of salary, whichever is less, for computing his taxable income.

Now all Employees will get a Standard Deduction of 50000 per annum

Hence,their Income will be reduced by 50000 while calculating tax

Benefit of Standard Deduction is only for Salaried Individuals(Not for those having Business Income)

Entertainment Allowance Section 16(ii)

Normally for allowances, the amount exempt is mentioned. However for entertainment allowance, deduction amount is provided in Income tax and not the exemption amount.

The total amount of Entertainment Allowance is first included in Gross Salary and then deduction is provided

Maximum deduction is lower of the following

- Actual amount received

- 20% of basic salary

- 5000

However, this deduction is provided only for Government employees. For Non Government employees it is fully taxable

Note :- Entertainment allowance is also called sumptuary allowance

Question 1

Basic salary Rs 20000 per month

Dearness allowance (DA) Rs 10000 per month

Entertainment allowance Rs 5000 per month

Calculate income from salary assuming employee is a Government Employee

View Answer| Particulars | Amt. read | Exempt | Taxable |

| Basic Salary | 240000 | 0 | 240000 |

| DA | 120000 | 0 | 120000 |

| Entertainment Allowance | 60000 | 0 | 60000 |

| Total (Gross Taxable Salary) | 420000 | 0 | 420000 |

| Less Deduction | |||

| Entertainment allowance | |||

| a – Actual amount received | 60000 | ||

| b − 20% of basic salary – | (240000x20 %) | 48000 | |

| c − Rs.5000 | 5000 | ||

|

Deduction u/s 16 (ii) for Entertainment Allowance Lower of a, b, c |

5000 | ||

| Income from salary | = 420000 – 5000 | 415000 | |

Question.2

Solve Question 1 assuming it a non government employee

View AnswerEntertainment Allowance will be included in Gross Taxable Salary

No deduction for entertainment allowance in this case

| Particulars | Amt. read | Exempt | Taxable |

| Basic Salary | 240000 | 0 | 240000 |

| DA | 120000 | 0 | 120000 |

| Entertainment Allowance | 60000 | 0 | 60000 |

| Total (Gross Taxable Salary) | 420000 | 0 | 420000 |

| Less deduction | |||

| Entertainment allowance | |||

| a – Actual amount received | 0 | ||

| b − 20% of basic salary – | 0 | ||

| c − Rs.5000 | 0 | ||

| Deduction u/s 16 (ii) is Lower of a, b, c | 0 | ||

| Income from salary | = 420000 – 5000 | 420000 | |

Professional tax / tax on employment Section 16(iii)

In some states in India, State Governments charge Professional Tax from the employees.

While In some companies, employers pay this professional tax from their pocket while in others they deduct it from employees salary.

In Income tax it is allowed as deduction and not exemption as shown below

If it is paid by employer

It is included in Total income as it is a benefit provided by company and then Deduction is provided

If it is paid by employee,

It is not included in Total Income as no money is received from employer .It is only allowed as deduction

Note:-

If professional tax is due but not paid, then it is not allowed as deduction

Question 1

Basic salary = Rs. 20000 per month

Professional tax = Rs. 500 per month

Calculate Income from salary if professional tax Paid by employer

View Answer| Particulars | Amt |

| Basic Salary (20000*12) | 240000 |

| Add professional tax (500*12) | 6000 |

| Gross Taxable Salary | 246000 |

| Less – Deductions for professional Tax | 6000 |

| Income from Salary | 240000 |

Question 2

Solve Question 1 assuming employee pays professional tax

View Answer| Particulars | Amt |

| Basic Salary | 240000 |

| Total | 240000 |

| Less – Deductions | |

| For professional tax | 6000 |

| Income form Salary | 234000 |

Hi, you can learn Accounts, Tax, GST, Tally from our website Teachoo (टीचू)

Click to learn

Tax

(TDS , Payroll , ITR-Income Tax Return , GST)

Excel

(Basic Excel , Shortcuts , Vlookup , Hlookup , Pivot Table , Macros)

Accounts

(Debit-Credit Rules, Entries , Balance Sheet , Fund Flow , Cash Flow , Ratios)

GST

(Basics , Computation , Returns , Registration , Challans)

Tally

(Basics , Ledger creation , Passing Entries , Tally Shortcuts)

You can also attend our Practical Training Classes. Click here to Register